Electricity producers and consumers value the predictability of the electricity price. Most electricity producers sell their future production in advance, an activity that is called electricity price risk hedging. In practice, hedging involves locking in the electricity price in advance through derivatives on the Nasdaq Commodities power exchange or through bilateral agreements. At the moment, more and more hedging is being done through bilateral agreements with other companies. Hedging on the exchange requires cash collateral, the logic of which is described in more detail here.

For example, when an electricity producer knows the future price of its product, thanks to hedging, it can better forecast its future cash flow and plan its operations and investments.

Fortum hedges electricity prices to minimise market risks

The key principle behind Fortum’s hedging activities is to minimise market risks. Explicitly: we do not engage in speculative trading. Hedging is done several years in advance to ensure future cash flows at a predictable level.

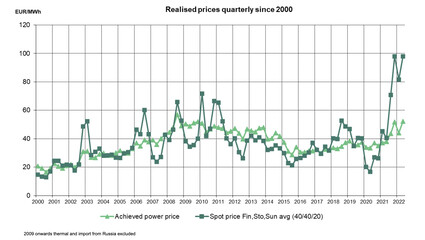

In the Nordic countries, the availability of hydropower has traditionally had a significant impact on the price of electricity. In dry years the price is higher, and in wet years the price falls. If we were to rely only on the spot price, cash flow could fluctuate quite a lot. The figure below shows the price Fortum receives for electricity with hedging compared to a situation without any hedging. Without hedging, our financial result would have fluctuated a lot and it would have been almost impossible to forecast cash flow.

Fortum hedges both its production and its purchases, but the hedging volume of production is significantly higher. There is a big difference in the amount of electricity production to be hedged and the quantities of electricity sold to consumers at a fixed price, and therefore the sales and purchases are not netted, as is the case with some smaller electricity companies, for example.

We regularly publish the hedging ratios of our Nordic production in the interim reports. In our most recent interim report, for instance, we said that 60% of our 2023 production is hedged at EUR 37/MWh. Fortum’s principle is that not all production is hedged. This is so that we can ensure our ability to also deliver all the electricity we have hedged – even at times when there is less hydropower available or a power plant is offline.

Own power plants behind Fortum’s derivatives agreements

Hedging is a long-term activity. For example, Fortum started selling the 2023 production already several years in advance. The hedging ratio then gradually increases over time towards the target level before the time of delivery. So the final hedge price is thus the average of individual trades made at market price over the longer term. In 2020, the electricity price on the wholesale market was about EUR 25/MWh for 2023; this year, it has been as high as EUR 284/MWh. In the recent rollercoaster market, we have actively and significantly decreased our hedging position on Nasdaq to curb the collateral requirements.

In terms of Fortum’s hedging activities, it’s worth keeping in mind that our own electricity production and our own power plants are always behind all our derivatives agreements. We hedge only as much as we are able to deliver with certainty in all circumstances.

Wishes for a crystal ball

The energy markets are in an unprecedented situation, the root cause of which is the war. Russia’s attack on Ukraine and the use of energy as a weapon has led to an energy crisis in Europe. Prices for energy commodities, including electricity, have soared many times over. The situation is causing difficulties for consumers, businesses and also energy producers. For example, the 2023 derivatives price of Nordic electricity has increased sixfold since Russia’s attack. We did not anticipate that, and the current market regulation is not designed for this kind of market.

The very high collateral requirements of the electricity exchanges are particularly challenging for electricity producers. Fortum is one of the biggest electricity producers in the Nordic market, so this issue is especially important to us. With a large production portfolio comes large collateral requirements. At their peak, our collateral requirements were about 5 billion euros based on the closing prices on 26.8.

Throughout the turmoil of recent months, many have wished for a crystal ball that would reveal the market’s next twists and turns. Alas, there is no such crystal ball, so we have to deal with the uncertainty of the markets. We hope for the best, but prepare for the worst. This preparedness is reflected in the aid packages for energy companies planned by the Finnish and Swedish governments. They strengthen financial resilience in the midst of volatility and provide security for any new twists and turns on the rollercoaster.